2026 Industrial Equity Capital Markets Mid-Year Update

A Record First Half for Industrial ECM and Expectations for a Strong Second Half

Our Industrial Equity Capital Markets team had the most active start to a year since 2021, successfully completing 20+ transactions and raising $13+ billion. The team sees the momentum continuing into the second half of 2026, supported by a strong pipeline of IPO engagements and follow-on opportunities. Equity markets have remained open despite recent choppiness, and we view the mid-summer pause as a natural reset before issuers return through the post-Labor Day window, where sustained investor appetite for high-quality industrial assets tied to defense, energy, infrastructure and space themes should drive a busy fall.

In this mid-year update, we recap key equity market trends and themes from the first half of 2026, highlight activity across the Industrial ECM landscape and share our outlook for the remainder of the year, including expectations for new issuance and sponsor-backed activity. The report also features perspectives from Baird's senior leadership.

- 41 Completed Industrial ECM Transactions

- $26+ Billion in Capital Raised

- Bookrunner on Over 80% of Industrial Transactions

- 10 Different Financial Sponsors

Select 2026 Baird Industrial Transactions

Mid-Year ECM Takeaways

The first half of 2026 was a record-setting period for U.S. equity markets including the industrial sector, headlined by a surge in large-scale issuers accessing the public markets at a pace not seen since 2021. Enthusiasm within the defense, space and AI-linked industrial segments fueled both new issuance and investor demand, even as periodic macro volatility created brief rather than sustained pauses in activity. A growing number of sponsors and companies have pursued dual-track processes to assess the valuations public markets are now providing relative to a sale. The pipeline of large buyout-backed issuers that have outgrown M&A as an exit option remains a primary driver heading into the second half, with the first half validating the public markets as a viable liquidity path at scale.

Industrial IPO Takeaways

The first half of 2026 produced 20+ Industrial IPOs, the strongest opening half on record and more than double the prior best. That six-month total has already eclipsed every full year of the past decade, putting 2026 on track to become the most active year for new issuance by a wide margin. Issuance has clustered around the market's most in-demand themes, spanning defense and space tech, AI-linked names in critical power generation and climate technology, and issuers demonstrating best-in-class fundamentals. Scale has been the defining feature of the reopening, with five billion-dollar-plus IPOs already priced in 2026 after only two IPOs clearing the $1 billion mark across 2024 and 2025 combined. The trend of large-scale issuers returning to the market is evident in 2026's average base deal size of $620 million, excluding SpaceX's historic $86 billion listing.

Investor demand across IPOs has been consistent, with ~73% of offerings pricing at or above the midpoint and many issuers upsizing following well-oversubscribed books. That strength has carried into the aftermarket, with a median first-day gain of roughly 14% signaling healthy investor appetite and constructive pricing dynamics. Strong investor demand has also drawn first-time sponsors to the public markets, including the upsized Arcline-backed Arxis IPO.

Industrial Follow-On Takeaways

Industrial follow-on momentum that started to build in the second half of 2025 carried through into 2026, with 30+ offerings pricing in the first half raising $12+ billion in capital and substantially outpacing the comparable period last year. With the increase in volume, aftermarket performance has also remained favorable, mirroring the strength seen in the 2026 IPO class, with median first-day gains of 4% and 30-day gains extending to 7%. The sustained positive performance across primary and secondary issuances, alongside a constructive market backdrop, has set up what could be a highly active second half of the year.

Among the offerings priced in 2026, two main themes have emerged among follow-on offerings. The first relates to strategic primary raises returning, as high-quality issuers tap strong stock performance to fund growth initiatives and strengthen the balance sheet, headlined by Baird's $1.4 billion left-lead offering for Kratos. The second features sponsors increasingly using the open market window to realize liquidity, with a meaningful share of this year's follow-ons carrying a secondary component. That push for liquidity has extended into the newest cohort of IPOs, where lockups have been released ahead of schedule on the back of strong post-listing appreciation.

Baird’s Senior Leadership Outlook Soundbites

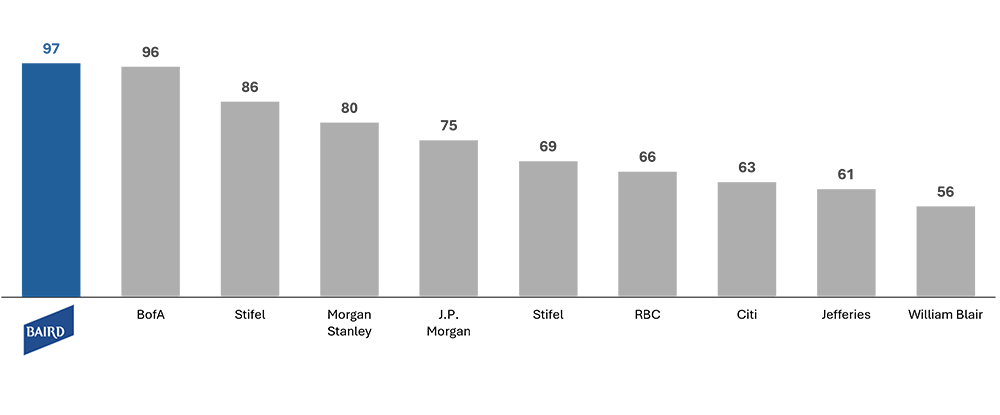

Leading Equity Underwriting Franchise since 2018 (1)