Baird Software Update: Better Days Ahead

With 2023 firmly in the rearview mirror, Baird’s Software team reflects on the year that was and provides perspectives on the year ahead

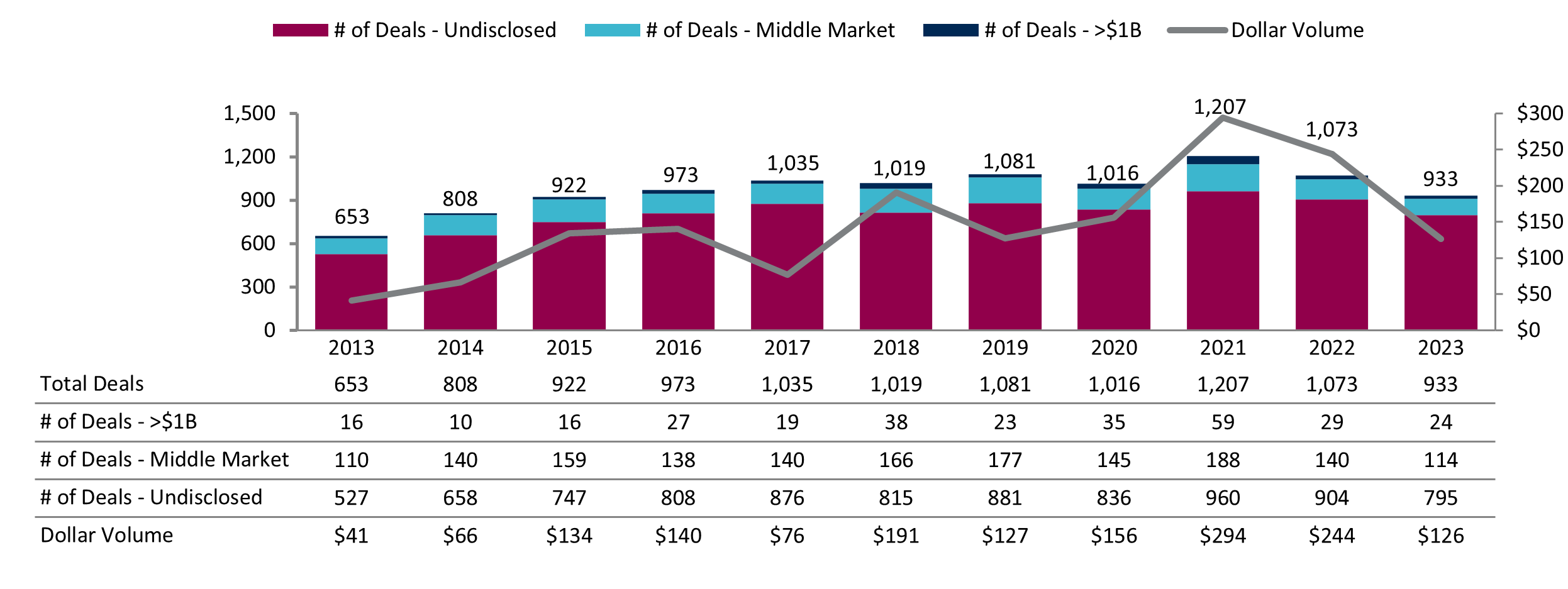

“A Tale of Two Markets” Dynamic Dominated the 2023 Software M&A Market

2023 was challenging year across the board for M&A in general, though sentiment and activity improved as the year progressed. In terms of deal count, the software M&A market in the U.S. saw similar challenges. Based on available data, 2023 deal volume remained well below the 2021 high watermark by ~22% and came in ~13% below 2022 levels. Dollar volume was down significantly, ~57% and ~48% lower than 2021 and 2022, respectively. Based on total deal count, 2023 volume came in below levels seen during the 2017-2020 stretch and rivaled levels seen in the earlier part of the decade.

Throughout the year, there were expectations of a broader market “re-opening” due to improved market conditions — these forecasts largely expected that post-Labor Day holiday there would be a “tidal wave” of deal activity. However, this did not come to fruition and the high-volume predictions turned into more of a slow and continual trickle, as sellers cautiously, but steadily tested the market.

In terms of the valuation environment, the software M&A market has seen a “tale of two markets” dynamic. In one way, the highest-quality, A+ assets have seen robust interest and are garnering valuation levels that rival 2021 multiples. Part of this trend has been driven by the high level of demand for software investments matched with the low level of available, actionable targets. Top tier software assets have enjoyed meaningful scarcity value (“flight to scarcity”). This has been coupled with investors seeking to rotate into safer, high-quality software businesses in durable end markets and out of cyclical, consumer discretionary stories (“flight to safety”). Outside of the top tier software assets, it’s been more challenging to pin a valuation trend versus 2021 multiples levels as deal activity has been lower, which is partially driven by transactions not getting done (due to inability to meet seller expectations or sellers electing not to go to market in favor of waiting for improved market conditions). The overall valuation environment improved throughout the year as the bid-ask spread between buyer and seller expectations narrowed to a constructive range. Sponsors that own majority positions in high quality assets have also been able to consider new paths to deliver DPI with constructs such as continuation vehicles and GP secondaries becoming a more popular route to a longer hold period.

Buyer scrutiny on cash flow and profitability has substantially increased in light of the need to meet debt service requirements. In the recent past, growth had a higher correlation to value versus profitability. In the current markets, growth plus profitability now has a higher correlation to value versus growth alone. While gross retention has always been an important consideration, we have also seen a high degree of scrutiny on the metric recently, particularly as investors conduct diligence on the criticality of targets’ solutions in light of concerns around the macro spending environment. Investors are leaning more towards higher gross retention rates 95%+, realizing that anything sub-90% shows evidence of a ‘leaky bucket’ and therefore require more work to control churn and renewal behavior rather than a more pure focus on new growth and / or upselling the customer base.

The take-private market continued to see robust activity as sponsors took advantage of historically low public market valuations on many assets; few publicly traded businesses fared well in the markets outside of the tech giants (‘The Magnificent 7’ stocks: AMZN, AAPL, GOOGL, META, MSFT, NVDA, and TSLA). While there was activity across-the-board, companies that had sub-optimal growth and cash-flow dynamics or businesses that were viewed as being particularly susceptible to a weaker spending environment attracted the most attention. We believe there remains a “private equity put” as financial sponsors are continually spending time evaluating publicly traded companies that might be undervalued or that sponsors believe can be better managed and upgraded in the private markets.

Software M&A Activity by Deal Size

Source: Capital IQ, Dealogic, and Robert W. Baird & Co. M&A Analysis. Table includes all announced deals with a U.S. based acquiror or U.S. based target.

European M&A Activity Followed the U.S. Trends with Volume Accelerating in Q4

In Europe, the software M&A market followed a similar pattern as the U.S. market, though it has generally been on a three-to-six-month lag versus the U.S. market. Q1 saw slightly lower deal activity versus the U.S. and then was followed by very low volume of activity in Q2 and Q3 (whereas the U.S. market was beginning to pick up). Similar to the U.S. market, there was a clear pickup in activity in Q4.

Lower middle market activity in Europe has been starting to see signs of rebounding, but larger deals have been sporadic. One notable exception is in take-private transactions, which have recently seen increased activity.

In Europe, the outlook for 2024 is steady with an expectation of a moderate increase in assets coming to market, which builds on the market momentum coming out of 2023. We expect the return of more traditional processes (rather than bilateral, off-market deals) as market participants have reacquainted themselves with the limitations of off-market deals, especially in an environment in which there are few pricing marks that give a sense for current market valuations.

Lending Markets Remain Supportive of Software M&A Activity

The ability to obtain debt financing was a key enabler for the software M&A deals that were completed in 2023. At the onset of the year, leverage levels across the market were suppressed due to increasing interest rates and fears of an impending recession. However, as the year progressed, both lenders and sponsors began to adapt to the “new normal” high interest rate environment and lender appetite gradually improved. Private credit funds (versus traditional bank lending) proved the most prominent source of financing for software transactions. This trend was underpinned by direct lenders’ record levels of dry powder and need to deploy capital and thus their willingness to get aggressive for top assets. In light of the interest rate environment, direct lenders put a premium on lending to assets with strong cash flow profiles and fixed charge coverage ratios (for EBITDA-based loans) or well-defined paths to profitability and ample cash cushions to cover debt service costs until that time (for ARR-based loans). Throughout the second half of 2023, lender confidence continued to improve and was further buoyed by the Fed’s December 2023 meeting in which they suggested an end to rate hikes and foreshadowed multiple rate cuts in 2024. As a result, ARR leverage levels for high quality software assets have improved to 2x – 2.5x+ ARR with pricing of ~S + 625 – 675, an improvement from their late 2022 / early 2023 trough levels, although still below the ranges reached in 2021. The outlook for lending markets in 2024 is one of cautious optimism: The bar for credit quality will remain high, but attractive financing packages will be available to high-quality credits.

Equity Markets are Positioned for a Return of Software IPOs

Equity markets outperformed in 2023 as moderating inflation, a strong labor market and generative AI optimism bolstered stocks. Major indices rallied into year-end after the Federal Reserve signaled the end of interest rate increases and recession fears abated in hopes of a soft landing. Technology and software were in favor as portfolio managers shifted their attention to growth sectors, and public companies experienced stabilizing demand trends, moderating growth and improving profitability. The IGV software ETF finished the year up 59% marking its best annual return since the index was established in 2001, while Technology-dominated Nasdaq closed the year up 43% with its best performance since 2020. However, performance was heavily influenced by a small number of stocks as the ‘Magnificent 7’ accounted for 63% of market value gains in the S&P 500. Volatility, as measured by the VIX index, remained low supporting broader market stability. The VIX averaged 16.9 compared to the 2016-2022 average of 19.1. Finally, stock market momentum also supported multiple recoveries with the IGV now trading at 8.2x NTM revenue. This valuation benchmark was last seen in January 2022 and is well above November 2022 lows of 5.5x. The recent increase in the equity market software valuations has provided constructive signals to the software M&A market and the overall valuation environment.

Source: Dealogic as of December 31, 2023.

The technology / software IPO market reopened in 2023 with three notable IPOs: Arm, Instacart and Klaviyo. All three issuers demonstrated category leadership in large markets and a combination of revenue scale and profitability. The transactions received broad investor participation, strong order book subscription rates of 10x – 30x covered and large anchor orders from long-only investors. All three issuers demonstrated category leadership in large markets and a combination of revenue scale and profitability. Aftermarket trading performance has been mixed, and other prospective issuers pushed launch timelines into this year in anticipation of better market conditions. With a broader rally in software and small / mid-cap stocks, the expectation is that 2024 will be more active. The IPO backlog remains robust as issuers on confidential file with the SEC closely watch market windows, conduct test-the-waters investor meetings and prepare for a public filing and roadshow. Early 2024 IPOs will continue to favor issuers with leading market positions, meaningful revenue scale, durable growth, and a compelling margin profile. In addition, a growing number of issuers looking for growth capital, acquisition currency or liquidity options for early shareholders and employees are expected to revisit IPO plans in 2024. Easing monetary policy and anticipated Fed rate cuts - coupled with an improving demand environment and a return to growth for software companies - are expected to further accelerate software equities momentum and attract more issuers to the public market.

Looking Forward to 2024

As 2024 gets underway, the early sentiment is we have a better setup for software-related deal activity than we had at this time last year. Most deal makers we are speaking with are feeling optimistic for increased M&A volume in 2024 and our leading indicators of pitch activity, backlog and deal launches support this outlook. Part of this dynamic is driven by the growing momentum that “sellers need to sell, and buyers need to buy,” which we believe is creating a more constructive M&A environment overall, but especially for software assets. In light of DPI-related considerations, private equity is receiving mounting pressure from LPs to create liquidity on investments. Further, private equity and corporate strategics are sitting on record amounts of dry powder that needs to be deployed. We expect best-in-class software assets will continue to garner very healthy valuations and be highly sought after, while the overall valuation for the broader software M&A market will become more constructive in 2024 than it has been in recent past.

Thank you for reviewing Baird’s Software Update. We expect robust deal activity in software in the near-term. Please do not hesitate to reach out to members of the Baird Software team to discuss how we can be helpful meeting your objectives.