Record Transatlantic M&A Activity Through Covid

US buyers reach new highs acquiring European targets, especially in the UK

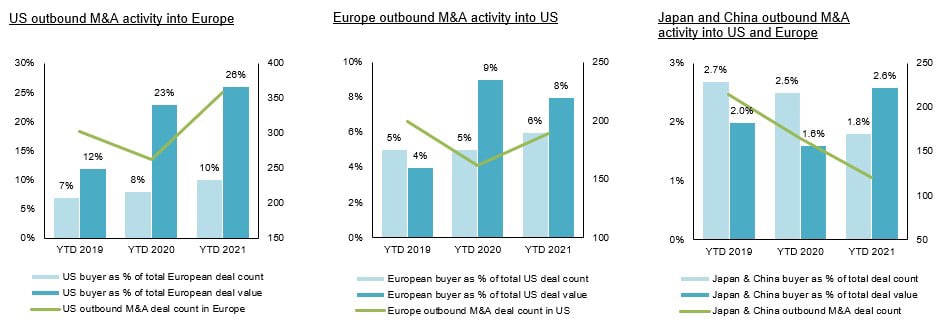

Transatlantic M&A activity flourished despite the ongoing coronavirus pandemic, continued international travel restrictions and repeated national lockdowns. The most notable increase relates to US outbound M&A activity, where US buyers accounted for a record 10% of total European deal count and over 25% of disclosed European deal value YTD (year to date) 2021, double pre-Covid levels in 2019. Since the start of 2020, the UK represented 35% of US to Europe M&A deal count and 70% of disclosed deal value, a record share compared to prior years.

Source: Dealogic as at end of May 2021.

Note: Deal values are total of disclosed EV deals only.

This surge in US to Europe M&A activity has been driven by:

- High public company valuations in the US, enabling valuation arbitrage when acquiring lower valued European targets

- Sizeable M&A deals by US listed SPACs acquiring in Europe, where there is little competition from European listed SPACs

- Continued globalisation and localised operations to address customer needs and strengthen supply chains across regions

Such factors are in addition to current M&A demand drivers:

- Proactively increasing exposure to secular growth themes

and non-cyclical / Covid-resilient businesses through M&A - Well capitalised corporates with $7tn of cash on balance sheets globally and record levels of PE (private equity) dry powder

- Strong debt markets in the US and Europe, with leverage and pricing at pre-Covid levels, supporting high M&A valuations

Furthermore, the supply of M&A targets is being driven by:

- Corporates divesting non-core businesses to optimise their portfolios and simplify the long-term equity story for investors

- Record number of PE portfolio companies, many of which are entertaining pre-emptive approaches from potential buyers

- Potential / upcoming increases to CGT (capital gains tax), accelerating shareholder decisions to launch sale processes

This relatively high velocity of cross-border activity since Covid has been supported by largely virtual execution of M&A transactions:

- Use of video conferencing and virtual site visits has shortened deal timelines and reduced expenses for buyers and sellers

- Fewer, higher value-added, in-person senior meetings eliminate unnecessary travel and efficiently focus management’s time

- Greater confidentiality allows sellers to engage with pre-emptive buyer approaches with a lower risk of rumours and market noise

While outbound M&A from Japan and China into the US and Europe has not recovered to pre-Covid levels, we expect robust transatlantic M&A to continue in H2 2021. The vaccine rollout and reopening of economies in Europe will increase M&A appetite for European corporates to acquire in the US. However, they may have to leverage synergies to compete with the high valuations offered by US corporates and PE firms in their home market.

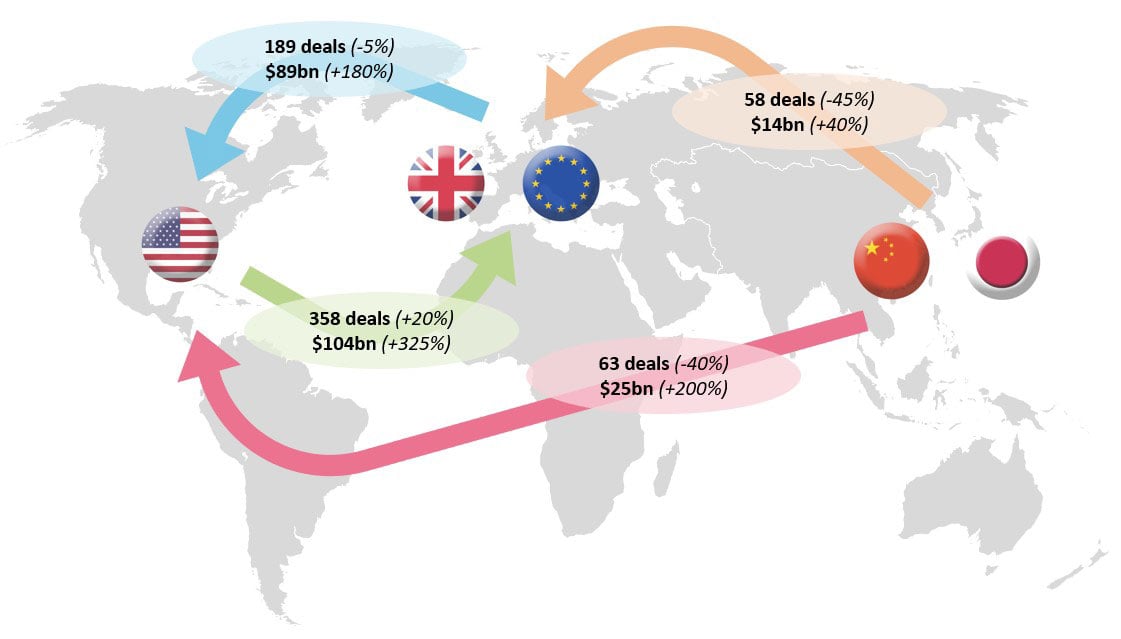

Key cross-border M&A flows (YTD 2021)

Source: Dealogic as at end of May 2021.

Note: Figures in brackets show change of YTD 2021 vs. YTD 2019.

Note: Deal values are total of disclosed EV deals only.

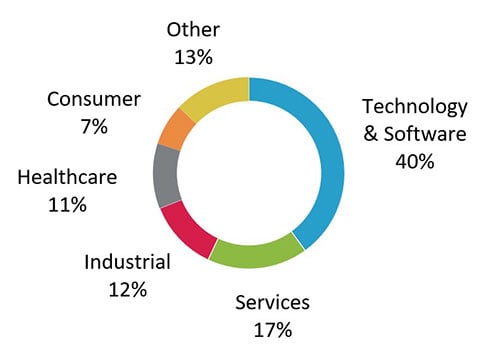

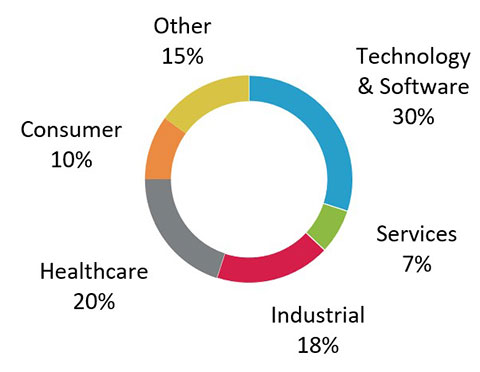

Transatlantic M&A activity by sector (YTD 2021)

M&A activity by sector in both directions across the Atlantic were similar in YTD 2021 with Technology & Software accounting for 40% of deals, up from 20% a decade ago. The share of Healthcare deals increased in 2020 and YTD 2021 relative to pre-Covid when it was two-thirds of its current share. Healthcare M&A from Europe to US is more active than US to Europe given the huge role of the private sector in US healthcare. The share of Industrial deals in both directions has decreased over the last decade. However, the share of Industrial deal value from US to Europe was 24% in YTD 2021, representing transformational M&A undertaken by US headquartered Industrial corporates.

US Outbound M&A Deal Count into Europe

Europe Outbound M&A Deal Count into US

Select US acquirers / targets in Europe >

>

Select European acquirers / targets in US

Source: Dealogic as at end of May 2021.

Note: Logos shown for select deals above $250m.

Asian outbound M&A activity to return from current lows

The two key countries in Asia for outbound M&A are Japan and China, with their activity peaking in 2019 and 2016 respectively. Since Covid, potential buyers from Japan and China have largely struggled to engage in competitive M&A processes in the US and Europe. Many of these processes have been for Covid-resilient businesses, often marketed to a narrow group of US and European potential buyers that have already expressed interest in the target. However, Japanese and Chinese buyers are successfully acquiring a number of larger targets in the US and Europe with disclosed outbound deal value substantially higher in YTD 2021 than YTD 2019.

The decline in Japan outbound M&A after 2019 was driven by:

- Covid related travel restrictions, when permitted e.g. 28 days of quarantine (14 days on arrival, 14 days on return)

- Cautious and slow vaccine rollout – only 8% of Japan’s population received at least one jab as of May 2021

- Covid-impacted sectors needing to focus internally and prioritise the recovery of their own business

The decline in China outbound M&A after 2016 was driven by:

- Stricter regulatory regime for capital outflows out of China

- Tighter regulations for inbound M&A into the US and Europe, especially for technology and infrastructure assets

- Covid related international travel restrictions since 2020

We expect Asian outbound M&A to increase over the medium term:

- Resumption of normal international travel, enabling in-person management meetings and physical site visits, a “must-have” for many Japanese corporate buyers before committing capital

- More willingness to participate in regular M&A processes to compete with US and European corporate acquirers and PE firms as business activity level increases

- Improved trading relationships between China and the US with the new Biden administration and between China and the EU with their signed Comprehensive Agreement on Investment

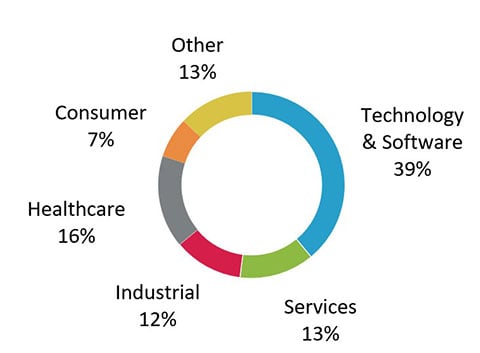

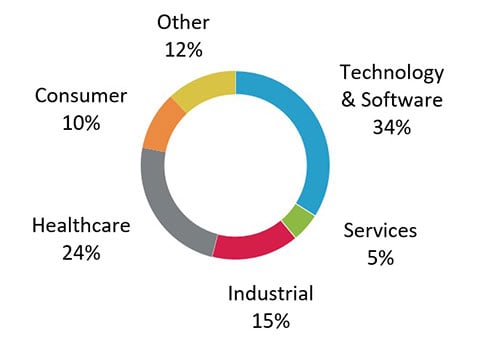

Asian outbound M&A activity by sector (YTD 2021)

M&A activity by sector from both Japan and China were similar in YTD 2021 with Technology & Software accounting for over 30% of deals, up from 20% a decade ago. Healthcare represented an average of 10% of outbound M&A by Japan and China over the last decade, and more than doubled its share to over 20% in YTD 2021. The share of Industrial deals decreased since Covid given the need for most Asian acquirers to hear the target management’s strategy and visit the key American and European facilities in person. In YTD 2021, there were double the number of disclosed outbound M&A transactions worth over $250m by Japan than China.

Japan outbound M&A deal count into US & Europe

Chinese outbound M&A deal count into US & Europe

Select Japanese acquirers / targets in US & Europe

Select Chinese acquirers / targets in US & Europe

Source: Dealogic as at end of May 2021.

Note: Logos shown for select deals above $250m for Japan and above $100m for China.