Death, Taxes and... Demographics

Benjamin Franklin is credited with saying, "In this world, nothing can be certain, except death and taxes." But savvy long-term investors know they can add demographics to the list.

With inflation annualizing at 7.9% (according to the Consumer Price Index), a 25 basis point increase in the Fed funds rate with six more likely on the way, the 10-year U.S. Treasury bond yielding roughly 2.4% and home mortgages rates over 4%, all eyes and ears are focused on the economic impact of a hike in interest rates. Yet two recent articles in The Economist suggest that the demographic trend of global aging is likely to keep a cap on interest rates over the longer term.

- How high will interest rates go? | The Economist

- Why the world is saving too much money for its own good | The Economist

My colleague Warren Pierson is Co-Chief Investment Officer at Baird Advisors, which manages $130 billion in bonds for institutional and individual investors. I asked for his take on the potential effect of U.S. age demographics on inflation. Here is what he had to say:

We believe/agree that aging populations and the associated increase in retiree savings will work to limit increases in interest rates around the world going forward. We think many strategists have continually underestimated/underappreciated the strength of these demographic trends. Retirees tend to save more and spend less and we believe that is part of the reason why the Fed's extraordinary stimulative policies over the last decade-plus did not produce the inflation that so many were eagerly anticipating. Instead of being lent and spent and greatly stimulating the economy, much of the easy money was simply invested and the only inflation that resulted (until recently) was in financial assets.

The COVID fiscal stimulus changed that as dollars were given directly to many individuals that had immediate needs who spent it, giving a big boost to our economy and creating demand-led inflation. While strong demand led to much of the inflation we are seeing now, a lot of the price increases (goods and labor) are more related to supply disruptions. While it is taking longer than expected to right many of these disruptions, we do believe market forces will correct them over time and inflation will eventually settle in much closer to the Fed's desired target of 2+%.

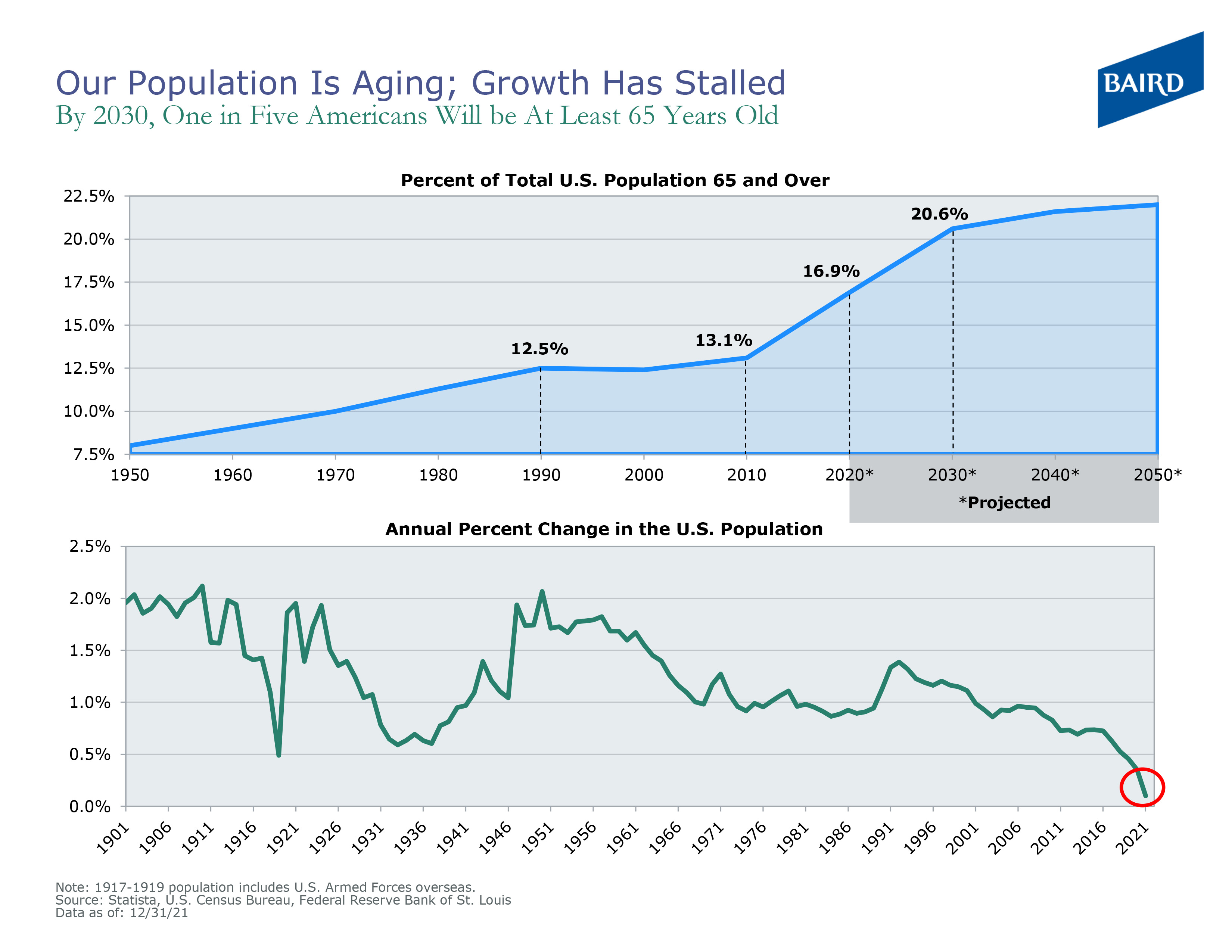

Another demographic consideration is the aging population's effect on the labor pool. Some estimates suggest that about 60,000 baby boomers are currently retiring each day in America. While that number might not be precisely accurate, the trend is clearly happening.

The chart below shows how the percentage of our population that is over 65 has grown and will continue to grow for the next decade plus. The lower panel also shows that our country's population overall is barely growing.

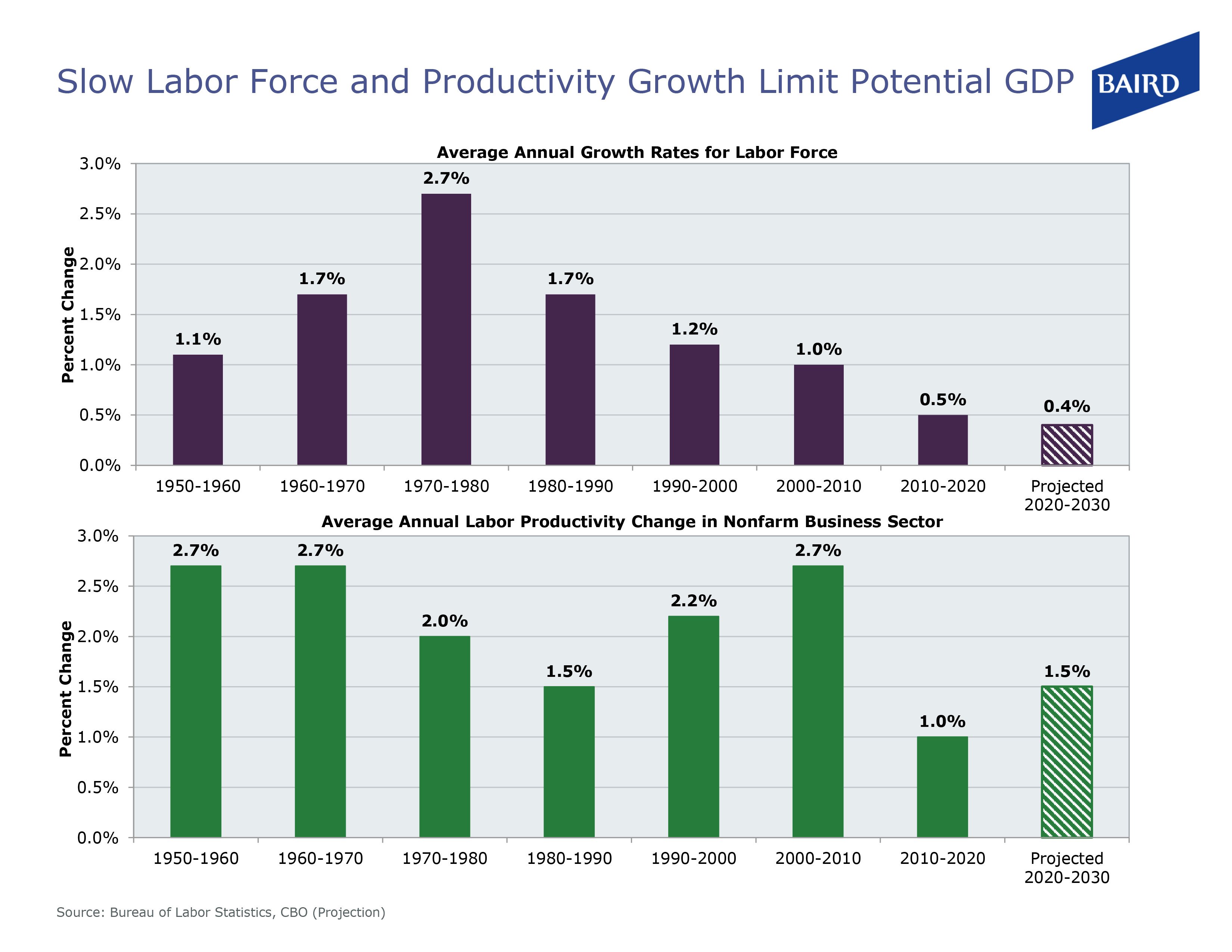

As a result, our labor force is barely growing (see top of chart below). Combining the growth in our labor force with productivity (bottom panel below) is another way of defining how fast our economy can grow.

Add these two estimates together and you get a long-term growth potential of about 2% – hardly inflationary. This is a major tenet of our thesis that interest rates will stay lower longer than many people think.

Many contend that the current environment feels a lot like the late '70s and early '80s. While we agree there are similarities in government policies, look at the difference in the large growth of our labor force from the '50s to the '80s. Not only was our country's population growing, but we also had many women leave their traditional homemaker roles and join the work force. That huge growth in the work force and big gains in productivity fueled much stronger growth that in turn led to higher inflation. We don't believe our economy has that same long-term inflation-generating potential for the foreseeable future.

What is the takeaway?

In the short run, the volume of retiring Boomers is contributing to a current labor shortage that is putting upward pressure on wages. Baird's take is that this increase in wages, which has been more focused on lower paying jobs, has been a very appropriate and much needed one-time adjustment or catch-up for workers whose wages have been largely stagnant for the past decade. We believe these wage gains will stick and hold. We also believe it is unlikely that such a large uptick will repeat. We feel the same about the price gains of many goods and services (e.g. cars, houses). That is, prices are not falling back, but also probably not advancing much further from current levels any time soon.

The evidence points to some significant differences between the cause of today's inflation and the factors at play in the 1970s, the period to which so many are drawing comparisons. The long-term effect of demographics is likely to be lower, not higher, interest rates.