Minimum Quantity: Order Protection vs. Venue Optimization

A Joint Study by Baird and IntelligentCross

Findings Challenge Conventional Wisdom Around MinQty

Reason for the Study

Robert W. Baird, Incorporated (“Baird”), in partnership with IntelligentCross (“INCR”), conducted a study of the effectiveness of Minimum Quantity (“MinQty”) tactics in Baird’s various algorithm configurations. We engaged IntelligentCross as a third-party resource to our views on MinQty instruction. The sample set of data used included seven trading days over a period of two quarters in 2019. The list was made up of full (non-holiday) trade dates and were randomly selected by the Excel random selection function.

At Baird, we strive to properly manage the balance between effective liquidity sourcing and market impact. Depending on the aggression level (algo strategy), stock, and/or market characteristics, we provide a menu of configurations to meet specific trader needs at the time of trade.

IntelligentCross operates Alternative Trading Systems (ATS) destinations IntelligentCross (mid-point) and IntelligentCross ASPEN^3 (bid/offer). As such, they were logical partners for Baird in this study sharing similar goals of minimizing market impact, but at the venue level.

Both Baird and IntelligentCross are dedicated to working with our customers to provide insightful ways of using our offerings to the best effect.

Minimum Quantity Refresher

FIX defines MinQty as the ‘minimum quantity of an order to be executed’. It was introduced in FIX3.0 (circa 1995) and has been widely adopted across platforms and venues.

- MinQty gives an order sender the ability to limit interaction with contra-orders below the specified minimum quantity value. For example, an order with MinQty of 100 will not execute against odd lots (sub 100 share quantities).

- MinQty is often seen as a defensive tactic with the goal of protecting larger orders from being discovered by trivial fills which can lead to information leakage and impactful market moves.

- MinQty utilization is still very common. INCR reports that, for Q1 2020, roughly 90% of their subscribers used MinQty on some portion of their order flow and close to 60% of mid-point and near side pegged ordered shares had MinQty specified.

Market microstructure has changed substantially since the introduction of FIX3.0. How has the use case for MinQty changed with it?

Executive Summary

After analyzing the data set, we summarize our findings as follows:

Protecting Single Orders

MinQty value as an effective tool to protect single orders is varied and situational.

- Usage of MinQty provides some level of markout* protection for near side pegged orders

- Evidence of MinQty protection for mid-point and far side limit orders is much less clear; and

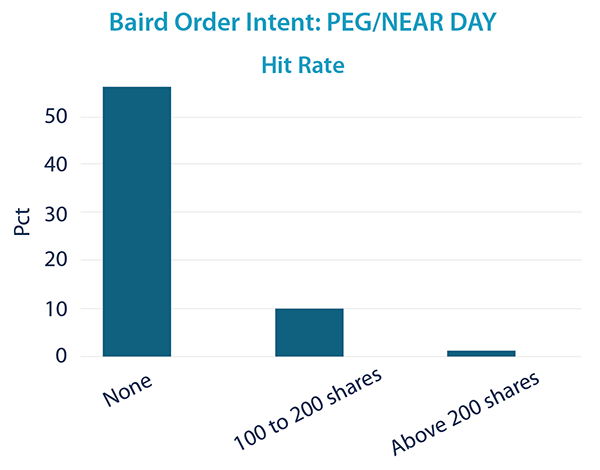

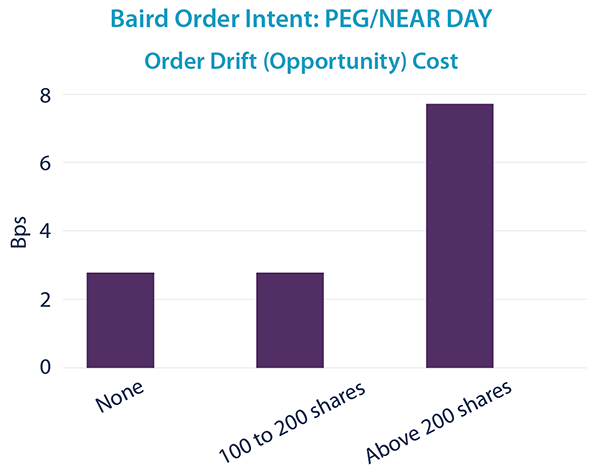

- Higher MinQty levels come with a substantial decay in hit rate and increased opportunity cost

* Markouts are measured as the absolute movement in mid to mid quotes from execution to some point in the future in bps, weighed by executed shares

Adding Value

MinQty adds value through venue optimization.

- Venues have persistent performance characteristics

- Utilizing a lower MinQty with “safer”** venues and a larger MinQty with less protective ones increases liquidity interaction while minimizing performance impact

**Where safer is defined as a tendency to show more stable prices for longer periods after a trade as measured by quote stability. The quote stability results were accessed through the Clearpool AMS, and measure the percentage of the time the quote was stable in various time buckets, both pre and post trade, on average over the life of the order.

-

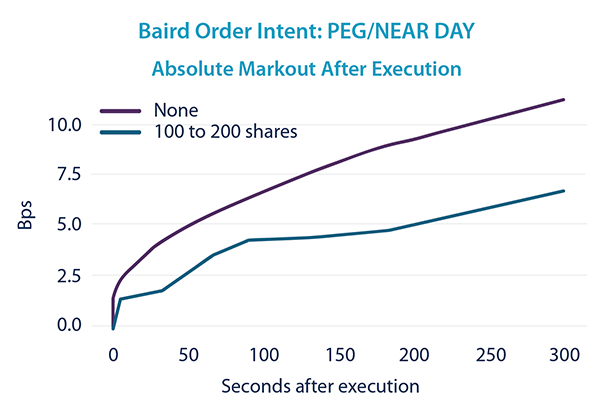

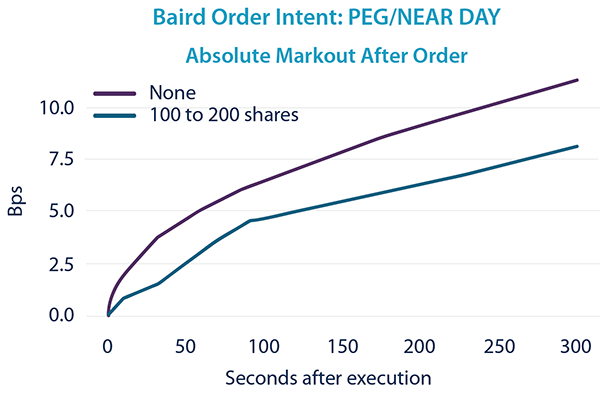

Near Touch Orders

Post-execution markouts monotonically increase, even up to 5 minutes out, on passive orders without MinQty versus those with MinQty.

Interestingly, markouts on unexecuted orders without MinQty have roughly the same markout as executions without MinQty.

This suggests lack of MinQty reflects urgency and potentially the short term “edge” of the order sender.

There does appear to be a muting effect on markouts for executions with MinQty versus both orders with and without MinQty and, potentially more importantly, versus orders with MinQty. T-Statistics are not definitive (pval of .19), but the use of MinQty seems to mute short-term market moves on near touch orders. However, this comes at a substantial cost in hit rate and order drift that, together, neutralize the gains in post execution markout. This suggests that MinQty is not, in isolation, a sufficient protection from information leakage for near touch orders.

-

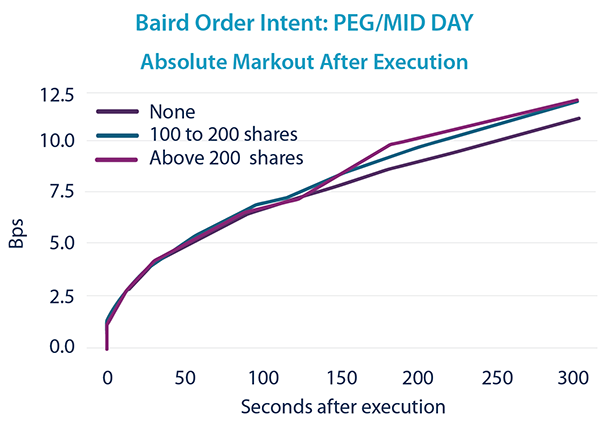

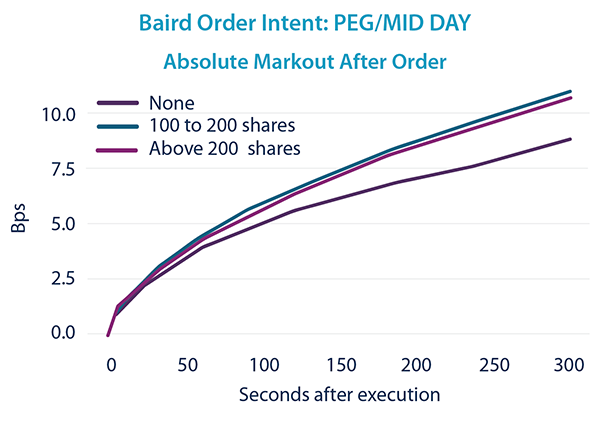

Midpoint Orders

Unlike near touch order flow, there is less distinction between using MinQty versus not for executions at midpoint.

Post-execution markouts are very similar across different MinQty levels, even up to 5 minutes out.

Interestingly, the muted markouts on unexecuted orders supports our intuition that the midpoint is typically used for more neutral flow and that the risk is in executions triggering any negative impact once they have gone to the tape.

Therefore, we attempt to preference “safer” midpoint venues such as IntelligentCross, IEX D-peg, and Nasdaq M-ELO that decouple matching from market events and show consistently higher post trade price stability.

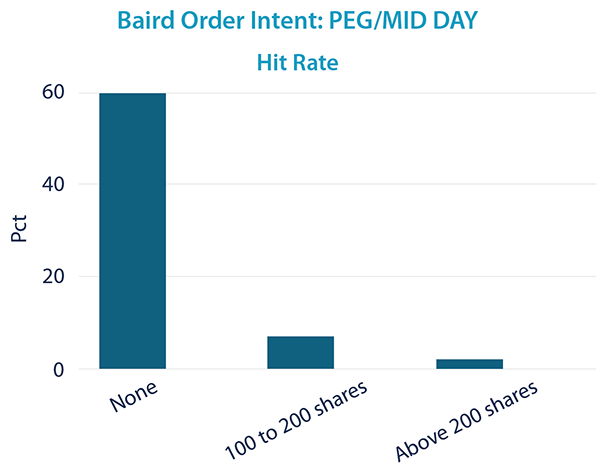

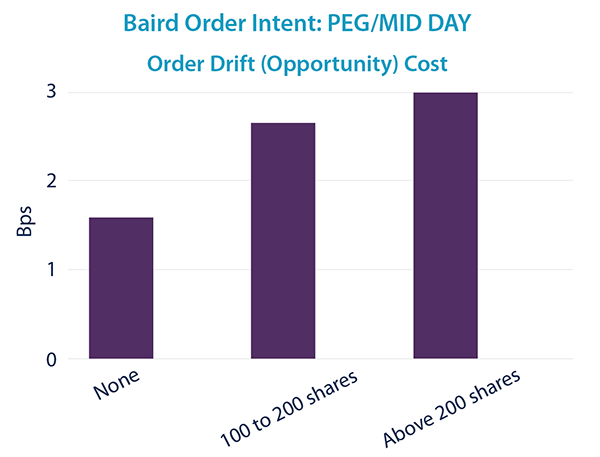

However, similar to near side orders, there is still substantial decay in hit rates and an increase in order drift that accompany the use of MinQty at midpoint.

-

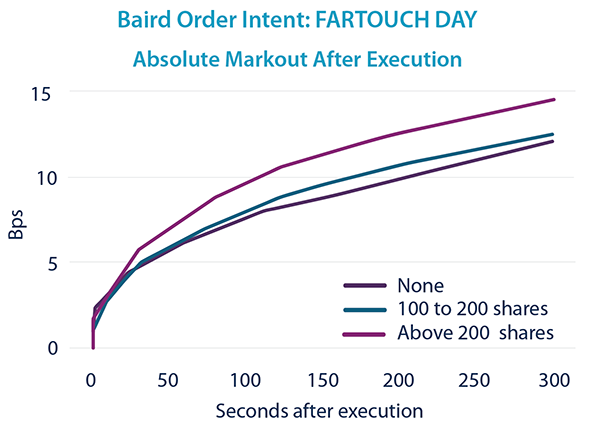

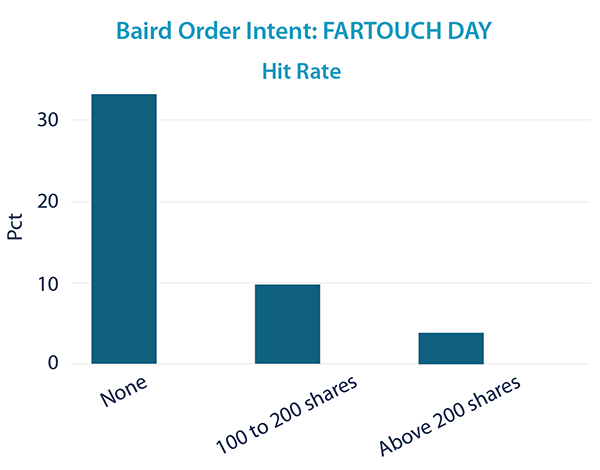

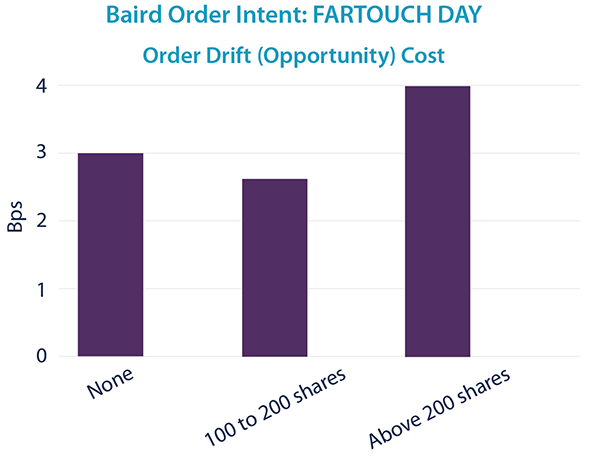

Far Touch Orders

Not surprisingly, far touch orders are, by their nature, urgent and are not afforded any distinct protection when utilizing MinQty. Markouts for executions with MinQty are comparable to, or greater than, those without MinQty.

However, as expected, far touch orders also have the highest markouts.

In addition, the decline in hit rate and increase in order drift from arrival time to cancel time suggests that attempts to protect markout with the use of MinQty ends up costing a full spread move by the arrival time of the next order.

-

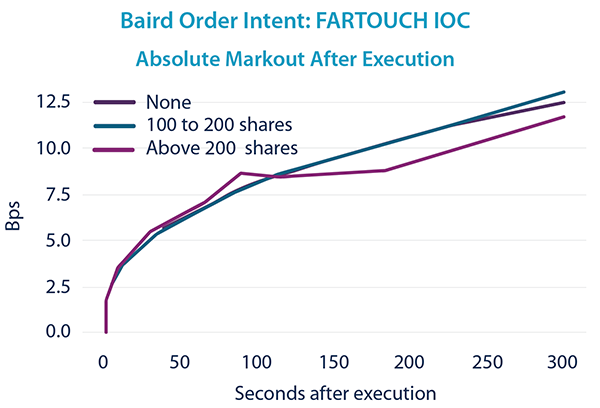

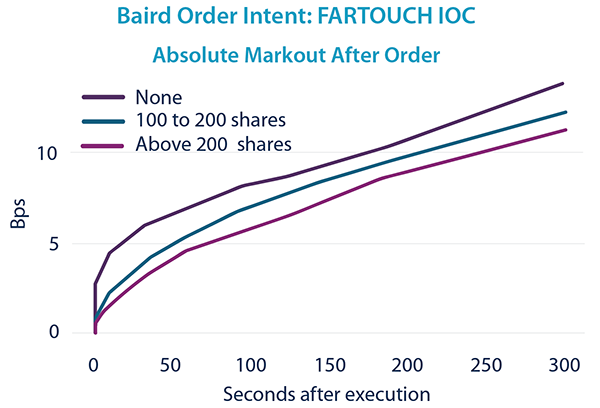

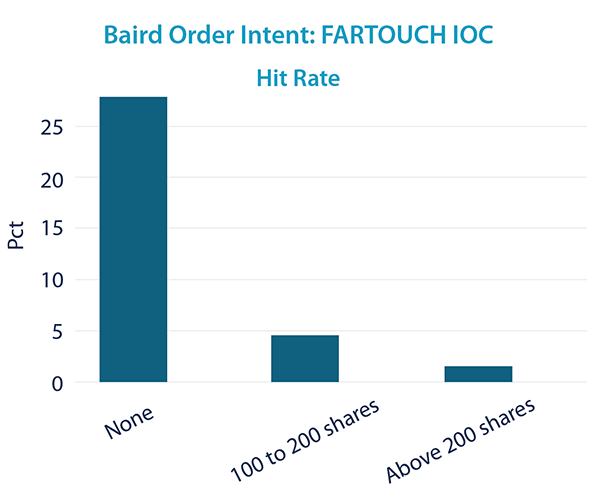

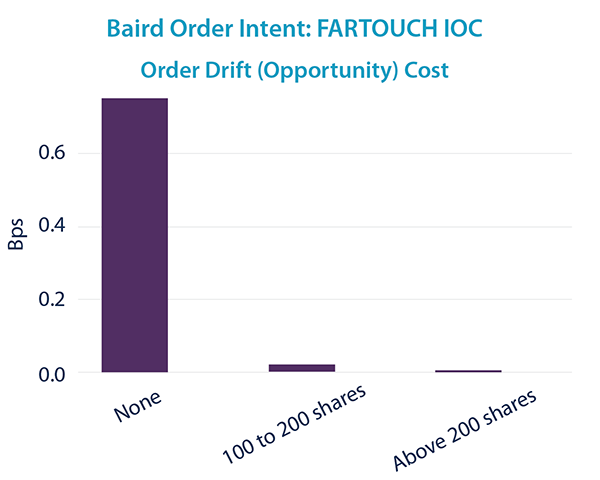

IOC Orders

IOC orders are similar to far touch orders in that MinQty does not seem to offer markout protection even though, on balance, zero MinQty orders tend to have higher expected markouts independent of execution.

Although hit rates drop substantially as MinQty increases, as in the case of all the limit types that we have reviewed, because of the short life cycle of IOC orders, there does not appear to be any significant opportunity cost to sending an IOC with a MinQty assuming that it is followed by a near simultaneous reload.

-

Initial Conclusions

From an overall limit urgency perspective (near touch, midpoint, and far touch), we find it difficult to make the case that MinQty utilization provides outsized protection against markouts when considering the decay in hit rate and the increase in opportunity cost due to order drift.

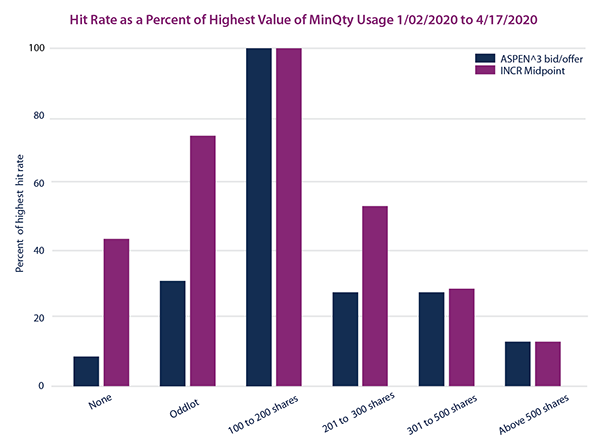

For example, IntelligentCross suggests that there is between a 40% and 60% cost to hit rate simply by increasing MinQty by 100 shares from the more optimal 100 share to 200 share range during Q1 2020.

The evidence shows that a broad “set-it-and-forget-it” approach to MinQty does not provide material value.

However, because MinQty can slow the speed of trading by decreasing liquidity interaction, it can add value as a filter at the venue level. Essentially, MinQty can enhance performance by acting as a venue optimization tool weighting venue safety vs. overall need for liquidity.

-

Minimum Quantity and Venue Optimizations

If we accept our suggestion that, for any given order, MinQty has limited protective value, how can we use it in venue optimization?

Venue optimization is the selection of trading venues through child order placement to maximize available liquidity while minimizing the implicit costs of trading such as impact.

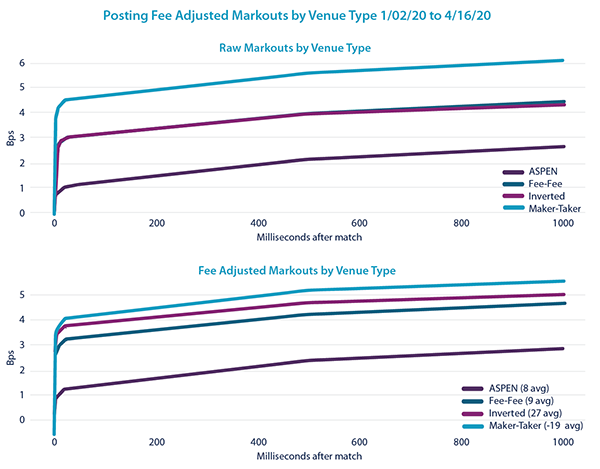

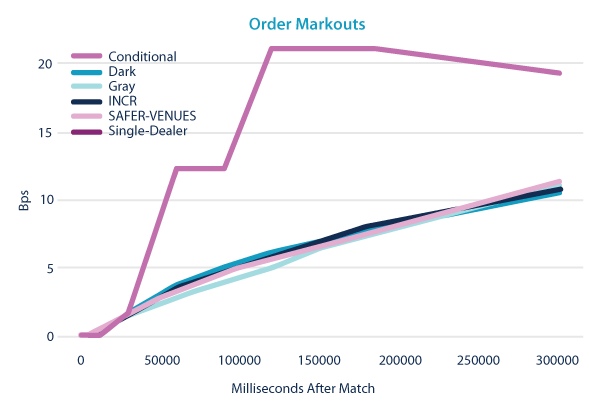

Venues have different and persistent performance characteristics. For example, as this plot from IntelligentCross shows, standard Maker-Taker venues typically have higher markouts than Inverted venues before accounting for fees.

Although venues can loosely fit into a spectrum of more or less safe as measured by post trade market movement, parent order benchmark performance is ultimately most sensitive to the percent of volume demanded.

There is little guarantee that safer venues can absorb the liquidity demands of larger institutional orders. Because MinQty allows the exchange of urgency for size, it allows us to be more urgent at safer destinations and less urgent at more volatile ones - increasing availability liquidity while prioritizing execution quality.

-

Venue Optimization in Action

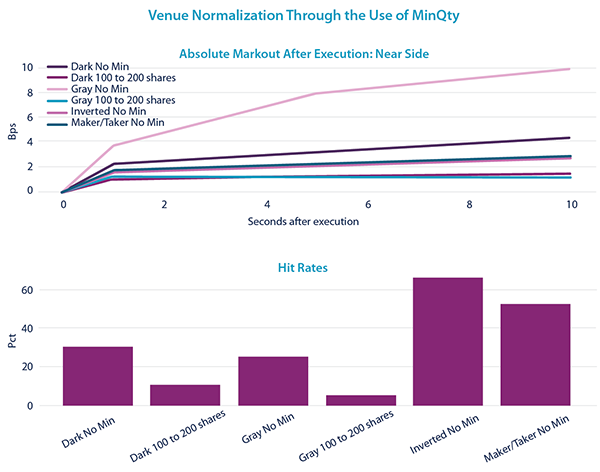

In our review of MinQty and order types, we saw that using MinQty was potentially beneficial for near side posting.

If we look at near touch order flow by venue type, we see that Dark and Gray venues without MinQty typically have higher markouts than Inverted and standard Maker/Taker venues similarly configured.

In this instance, Dark and Gray are an amalgam of “hidden” venues and not just destinations with a reputation for minimal impact.

However, by imposing minimum MinQty of 100 shares to 200 shares on those venues, we can bring overall performance in line with our highest performing venues while simultaneously increasing liquidity.

This idea of a minimum MinQty being sufficient loosely comports with a March 2018 study conducted by IEX D-peg. The study pointed out that while adjustment of MinQty based on stock characteristics was likely superior to other approaches, even the least aggressive setting provided sufficient protection.

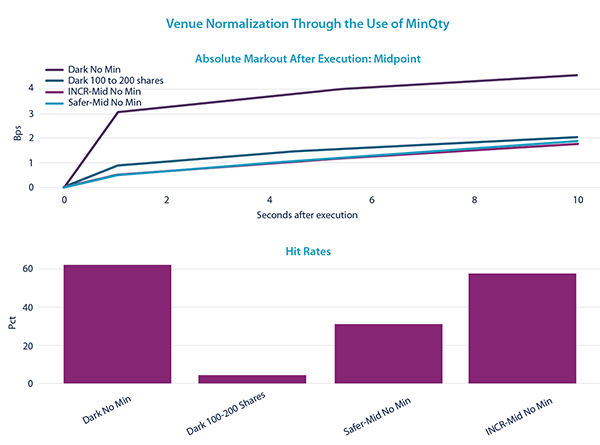

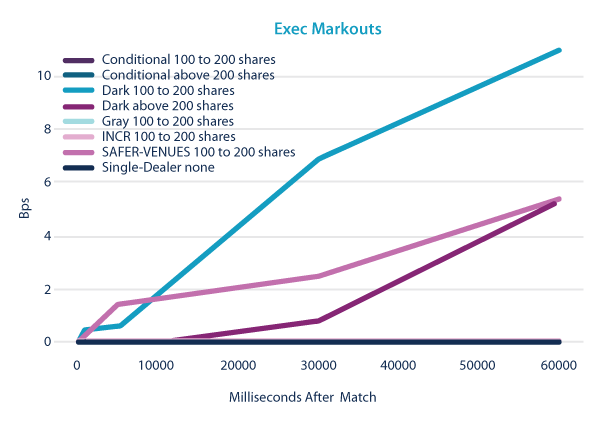

We see similar benefits to utilizing MinQty to access more liquidity in the midpoint context as well.

While protective mid-point venues, such as IntelligentCross, IEX D-peg, and Nasdaq Nasdaq M-ELO, typically have low post-execution signalling, other dark destinations can have substantial leakage. This is shown in the plot looking at post-execution Dark performance with no MinQty.

However, by adjusting MinQty to a minimum of 100 shares to 200 shares, we see post-execution performance in those venues more closely aligned with the “safer,” or more protective, mid-point destinations.

In this way, we can balance incremental liquidity with performance by sourcing as much liquidity as possible from unrestricted orders in protective pools while accepting the decline in hit rate to add additional liquidity from less protective pools.

Final Conclusions

MinQty, on its own, is of mixed value in protecting executions against poor performance

- Evidence that executions with MinQty outperform executions without MinQty is tepid and declines with an order’s urgency and willingness to be aggressive

- The cost in hit rate and order drift often outweighs any direct protection MinQty can provide

As such, MinQty should not be used as a generic defense tool

- It may not be an appropriate protection mechanism based on the trading context

That said, MinQty can act as a venue optimizer

- Venues show consistent post-execution performance characteristics

- Protective venues do not offer an infinite supply of liquidity

Therefore, using a lower MinQty on more protective venues and a higher MinQty on less protective venues provides balanced liquidity sourcing across available destinations

- How we use MinQty depends on how aggressively we want our algorithms to search for liquidity in a specific routing table and for that specific venue

Putting It All Together

IOC orders are similar to far touch orders in that MinQty does not seem to offer markout protection even though, on balance, zero MinQty orders tend to have higher expected markouts independent of execution.

Although hit rates drop substantially as MinQty increases, as in the case of all the limit types that we have reviewed, because of the short life cycle of IOC orders, there does not appear to be any significant opportunity cost to sending an IOC with a MinQty assuming that it is followed by a near simultaneous reload.

Applying These Findings

At Baird, we strive to provide the proper balance between efficient liquidity sourcing and market impact. MinQty settings are one of the tools that we use to achieve that balance. We also use liquidity segmentation to control counterparty interaction within a specific ATS, as well as specific differences in the routing tables themselves (where we route and how we route).

Specifically with MinQty settings, we do not use a “one-size-fits-all” approach. For venues that have built-in order protection, such as IntelligentCross, IEX D-peg, and Nasdaq M-ELO, we do not use MinQty. For standard ATSs, we adjust MinQty settings based on a number of factors such as toxicity scores, reversion, impact, urgency, etc.

Getting this formula right is not always easy. It is part art and part science. It takes a long-term data view and real-time (order-by-order) analysis. But as our tools become more robust, and our data analysis more detailed, we continue to gather the necessary intelligence to inform appropriate algorithmic adjustment decisions and to properly align client objectives with best execution results.

About Us

Baird: Established in 1919, Baird is an employee-owned, privately held wealth management, investment banking, asset management, and private equity firm with more than 200 offices and over 4,600 employees in the United States, Europe, and Asia. Baird has more than $300 billion in client assets worldwide. Since 2004, Baird has been recognized annually as one of the Fortune 100 Best Companies to Work For®. Quality. Consistency. Partnership. Baird.

IntelligentCross: IntelligentCross operates two matching books in its ATS - INCR. Intelligent Midpoint works to actively minimize market response after trades. ASPEN (Adverse Selection Protection Engine) Bid/Offer book, is fine-tuned for posting passive liquidity. INCR matches roughly 25mm shares single counted per day. For more information please email info@intelligentcross.com.

The corresponding material has been prepared by an institutional trader, sales person or desk analyst of Robert W. Baird & Co. Incorporated (Baird) and not by Baird's Research Department. The material is intended for institutional investors only. Recipients of this communication may not distribute it to others without our express prior consent. This communication is provided for informational purposes only and is not an offer, recommendation or solicitation to buy or sell any security. This communication does not constitute, nor should it be regarded as, investment research or a research report or securities recommendation, and it does not provide information reasonably sufficient upon which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Additional analysis would be required to make an investment decision and investors should independently evaluate particular investments and strategies. The opinions expressed here reflect our judgment at this date and are subject to change. The opinions expressed include our current views with respect to future events. Actual results may differ materially from our expressed expectations. The information in this communication has been obtained from sources we consider to be reliable, but we cannot guarantee its accuracy. The accuracy of the corresponding information has not been verified or confirmed; accordingly, no representation or warranty, expressed or otherwise, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or timeliness of the information. The observations or views expressed in the material may be changed by the institutional trader, sales person or desk analyst at any time without notice. The information is current only as of the date of this communication and we do not undertake to update or revise such information following such date. The material may have previously been communicated to Baird's trading desk or other Baird clients. You should assume that Baird makes markets and/or currently maintains positions in some or all of the securities mentioned in the material. In addition, the individual providing their observations or views on such securities may be personally responsible for making a market in such securities or in buying or selling such securities for Baird's proprietary accounts. Baird may also provide services or solicit business from, or participate or invest in transactions with, or effect transactions for the issuers of the securities mentioned in the material. The material is merely intended to provide the personal observations or views of individual institutional traders, sales persons, or desk analysts which may be different from or inconsistent with the observations and views of Baird's research analysts, other Baird institutional traders, sales persons or desk analysts or the proprietary positions held by Baird.