Download the PDF version Download the PDF version

Baird Advisors Fixed Income Market Commentary

August 2009

|

|

Treasury Yields Slightly Lower

|

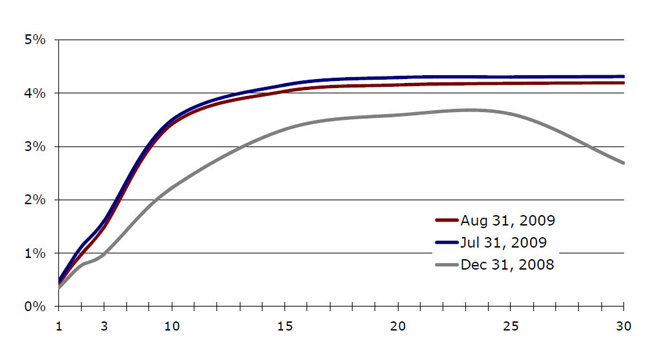

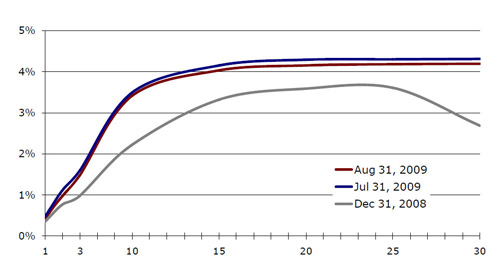

Treasury yields were volatile once again in August (10-yr. yield rose to a high of 3.85% on 8/7 from 3.48% on 7/31 and then fell to a low of 3.40% on 8/31), but finished the month slightly lower (down 5-15 bps) on concerns that declines in the Chinese stock market (down 6.8% from 8/11 to 8/31) would spread around the globe. The decline in yields came in the face very heavy new supply: the Treasury auctioned over $198 billion of notes and bonds and $624 billion of bills during the month of August. The shape of the curve did not change appreciably in August, but has clearly steepened so far this year (see chart and table below). |

Treasury Yield Curve Comparison

Source: Bloomberg |

Click for larger view

|

Maturity |

Dec 31, 2008 |

Jul 31, 2009 |

Aug 31, 2009 |

YTD Change |

1 |

0.34% |

0.47% |

0.42% |

0.08 |

2 |

0.76% |

1.11% |

0.97% |

0.21 |

3 |

0.97% |

1.59% |

1.47% |

0.50 |

5 |

1.55% |

2.51% |

2.39% |

0.84 |

10 |

2.21% |

3.48% |

3.40% |

1.19 |

30 |

2.68% |

4.30% |

4.18% |

1.50 |

|

Corporate Spreads Grind Together

|

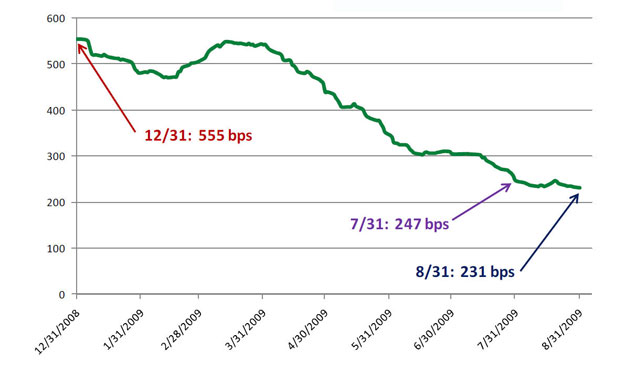

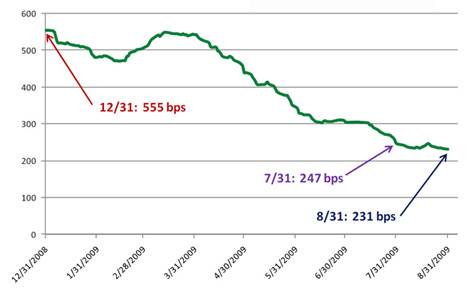

Corporate spreads continued to grind tighter in August (231 bps on 8/31 vs. 247 bps on 7/31) as strong demand from investors looking for yield has cut corporate spreads in half this year (see chart at right). New issuance of investment grade debt in August of $55 billion was slightly below this year’s monthly average of $78 billion, but YTD issuance of over $624 billion through the first 8 months of 2009 has already surpassed last year’s all-time record supply of $608 billion for any full calendar year.

|

Investment Grade Corporate Spreads (bps)

Click for larger view

|

Strong Returns

|

The decline in Treasury yields and compression of yield spreads resulted into strong returns for the bond market again in August. Asset-backeds (ABS) led all investment grade sectors this month (+2.37%) as they have so far this year (+20.81 % YTD) followed by corporates (+1.83%) and municipals (+1.71%). Government Agencies (+0.59%) and Agency MBS (+0.67%), which are shorter in duration, basically marked time with Treasuries (+0.89%) as did TIPS (+0.88%). High yield bonds posted another strong month (+1.86) and are rebounding much like stocks this year (+40.95% YTD). Please see sector and index returns in the table below.

|

Total Returns of Selected Barclays Capital Indices and Subsectors

|

Index/Sector |

August |

YTD |

| BC Aggregate Index |

1.04% |

4.62% |

| BC Gov’t/Credit Index |

1.18% |

3.56% |

| BC Int. Gov’t/Credit Index |

0.99% |

4.04% |

| BC 1-3 yr. Gov’t/Credit Index |

0.53% |

3.03% |

| US Treasury Sector |

0.89% |

-3.05% |

| Gov’t Agency Sector |

0.59% |

1.29% |

| Corporate Sector |

1.83% |

15.06% |

| MBS Sector |

0.67% |

4.45% |

| ABS Sector |

2.37% |

20.81% |

| High Yield Sector |

1.86% |

40.95% |

| Municipal Sector |

1.71% |

10.06% |

| TIPS |

0.88% |

7.22% |

|

Indices and subsectors are unmanaged and an investment cannot be made directly in an index or a sector . |