European PE Are Cautiously Optimistic for 2023

Following H2 2022 slowdown, a recovery may come later in 2023, supported by a large supply of already mandated targets

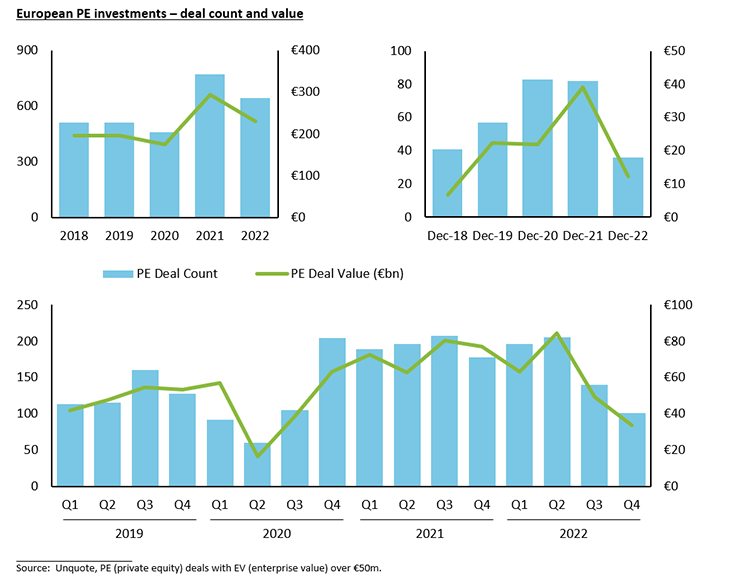

- European PE investments fell 40% in H2 2022 after a strong H1, falling more than the overall M&A market

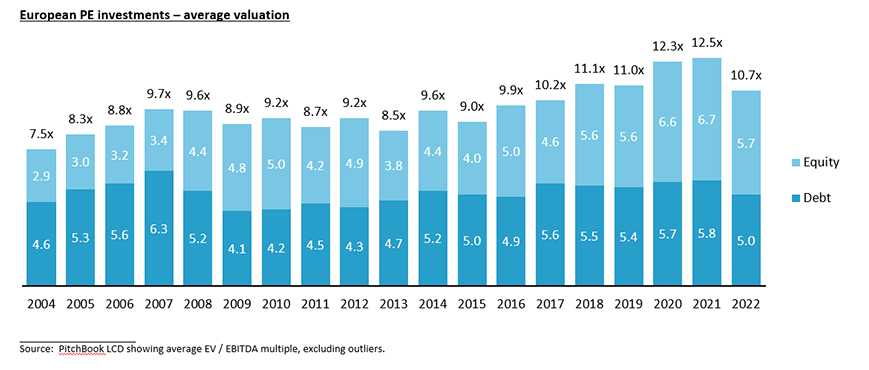

- Average LBO valuation decreased from record 12.5x EBITDA in 2021 to 10.7x in 2022, back to pre-Covid levels

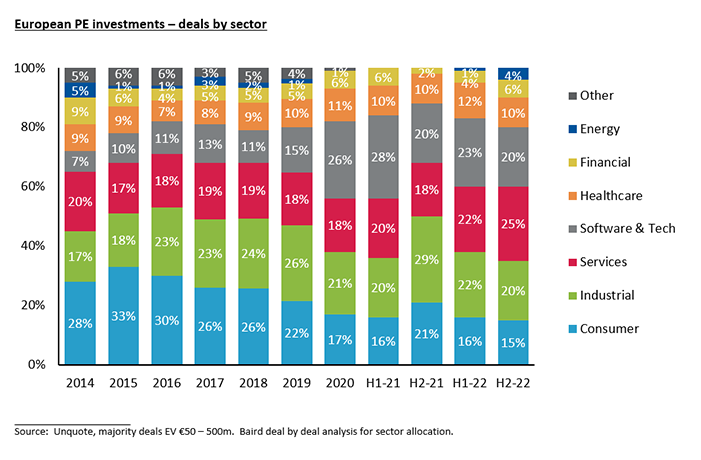

- Bifurcated sector activity in H2 2022 with services accounting for a record high share and consumer a record low – software & technology and healthcare now make up 30% of activity, a step-change increase from 20% pre-2019

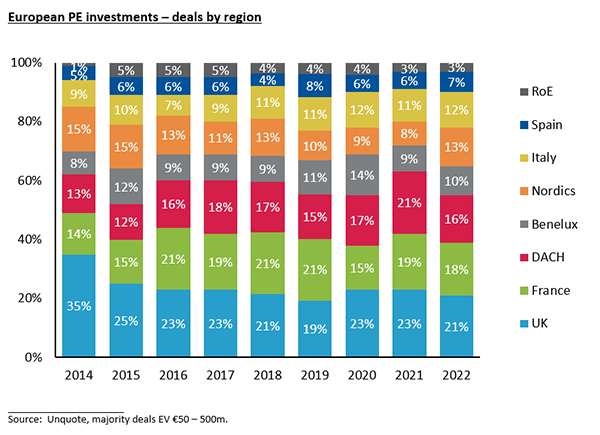

- The UK remains the most active PE investment region by deal count and value, followed by France and DACH

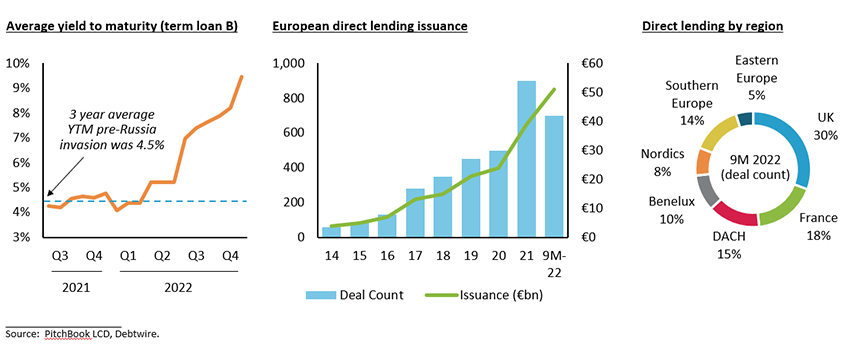

- European debt funds supported PE activity in 2022 and partially filled the void left by the syndicated loan market, though overall unitranche interest cost is now ~10% with debt capacity constrained to ~5x EBITDA for most credits

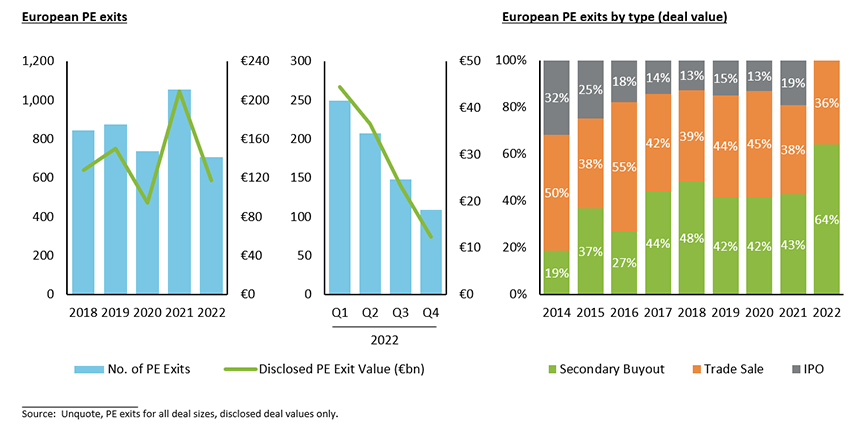

- PE exits down 50% in H2 2022 vs. H2 2021 as many sellers wait for improved macro and financing conditions

- Lower public company valuations drove significant public-to-private activity and no sponsor backed IPOs in 2022

- European buyout fundraising in 2022 was 30% down from 2021 – while the average fund size grew, the market continued to bifurcate as larger PE funds, with a successful track record, took a bigger share of LP commitments

- Reaching inflexion points for the macroeconomic outlook and public equity and debt markets could accelerate PE M&A later in 2023 (similar to H2 2020), unlocking a large supply of targets, many of which are already mandated

- Closer valuation alignment among buyers and sellers across broad base of sectors would support M&A recovery

PE deployment fell 40% in H2 2022 vs. H1 2022, but only 15% down on H2 2019

2022 was a year of two halves for the overall European M&A market – H1 2022 continued the strong deal momentum of 2021, while deal count decreased by 24% in H2 2022. European mid-market private equity deal count and deal value saw a steeper drop, falling 40% and 44% respectively in H2 compared to H1 2022. Unprecedented inflationary pressures, supply chain disruption and the invasion of Ukraine by Russia in February 2022 did not materially impact PE deployment in H1 2022. However, the expected European recession, cost of living / energy crisis and the increased cost and lower availability of debt financing negatively impacted PE deployment in Q3 and especially Q4 2022.

We expect 2023 to be a year of transition for private equity as the era of “cheap money” comes to an end and the industry adjusts to a new age of more normalised interest rates. Nevertheless, private equity is a deep and liquid market now relative to prior economic downturns, with proven ability to transact in changing macro environments, including Covid. While the number of PE deals in Q1 2023 is expected to be lower than in Q1 2022, we anticipate a substantial proportion to involve top-quartile assets in resilient sectors. PE deal momentum will likely be more active in the middle-market than large cap, which should pick up activity once the syndicated loan markets open more broadly.

PE exits down 50% in H2 2022 as many sellers wait for improved macro and financing conditions

The fall in PE exit activity reflects a decision by sponsors not to attempt to sell many of the portfolio companies that were earmarked for sale in 2022 in H2 2022. Disclosed PE exit value fell by 80% in Q4 2022 compared to Q4 2021, primarily due to difficulties for sponsor buyers to obtain financing for deals over €1bn. Debt funds were able to finance larger deals in the absence of syndicated loans and, while reducing the size of tickets as the year wore on, they were able to club with other debt funds. Many PE firms continued to launch and conclude sale processes in H2 2022 that had certain characteristics:

- High quality recession-resilient assets that garner significant buyer interest through economic and M&A cycles

- “Must-have” strategic platforms for corporate acquirers, potentially also benefitting from realisable synergies

- Company / sector specific factors e.g. secular growth trends supporting robust current and forecast financial results

- Shareholder specific factors e.g. liquidity event before fundraising, last portfolio company within an older fund, etc.

Unlike the US, the share of the “trade sale” exit route in Europe did not rise in H2 2022. Cash-rich strategic acquirers, not dependent on debt financing, may benefit from from lower competition from potential sponsor buyers in 2023. This dynamic of narrower or “strategic-only” M&A processes will allow strategic acquirers to spend more time (and money) on due diligence relative to prior years where some corporates struggled to be as fast and deliverable as PE buyers.

Like the US, European IPO activity fell 75% in 2022 as public equity markets suffered their worst performance in years. 2022 represented the first year in over two decades where there were no major sponsor backed IPOs in Europe.

Growth in alternative PE monetisation strategies – continuation vehicles and partial stake transactions

We are seeing a growing number of PE firms opt for continuation vehicles or partial stake transactions over traditional 100% PE exits to maximise returns for GPs and LPs over the long term through peaks and troughs of the M&A cycle.

Continuation vehicles (aka GP-led secondary sales) enable sponsors to address fund / LP liquidity considerations, raise incremental dry powder to pursue M&A, crystalise carried interest and retain future upside. In most instances, these transactions do not trigger a change of control, and the existing debt is portable, which means PE firms are not reliant upon the debt financing markets, further making this an attractive alternative to a sale in today's macro environment.

We are also seeing demand for majority stake M&A sales to another sponsor with the selling PE firm retaining a minority interest. This continued investment by the PE vendor helps bridge any potential gap in financing capital and provides a welcome reassurance to the investment committee of the acquiring sponsor.

In addition, PE firms are utilising minority equity recapitalisations to lengthen ownership periods and raise growth capital for favoured assets, allowing partial monetisation without having to undertake a debt refinancing. Having said this, minority equity recaps are often combined with debt financing (with incumbent lenders or new sources), structured equity (hybrid securities with elements of equity and debt) or continuation vehicles to optimise the capital structure.

Average LBO valuation decreased to 10.7x EBITDA in 2022, back to pre-Covid levels

European LBOs were completed at a lower average valuation in 2022, reflecting higher interest rates, lower leverage levels, reduced public market multiples and mounting buyer concerns about the impact of a recession on the target’s financial performance. Average valuation levels for European public equity markets (e.g. MSCI Europe Index) fell 25% during the course of 2022 compared to 15% for average European LBO valuation levels – closer valuation alignment among buyers and sellers across a broad base of sectors would support a sustained M&A recovery.

Having said this, valuation levels for top-quartile assets of scale in resilient sectors remain elevated given the continued “flight to quality” we have seen through Brexit, Covid and today’s recessionary environment. Indeed, the median EBITDA multiple in 2022 for Baird’s completed sell-sides, primarily middle-market PE exits, matched the record level of 2021, benefitting from continued strength in buyer demand for best-in-class business models.

Bifurcated sector activity in H2 2022 with record highs and record lows

Mid-market PE investments by sector in H2 2022 reflected a mix not seen before. Though all sectors saw reduced deal activity in H2 2022, the 25% share of services deal count was a record high while the 15% share of consumer was a record low. PE buyers and lenders alike focused on services business models with long term customer contracts and strong net retention rates such as FIRE (facility, industrial, rental and environmental) as well as exposure to secular growth trends such as GRC (governance, risk & compliance) and ESG (environmental, social, governance).

The 20% share of software & technology deals in H2 2022 likely represents the “new normal” for the European PE market. Highly profitable software companies saw robust PE buyer interest compared to earlier stage tech companies that have seen a reset in valuation levels following declines of up to 50% for Big Tech in public market capitalisations.

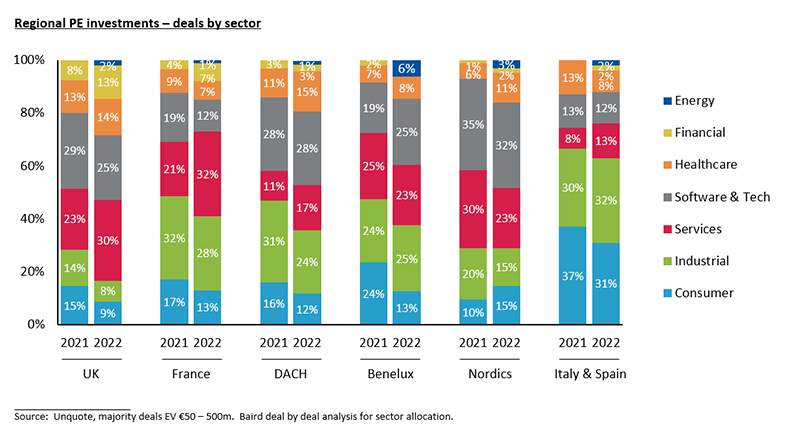

Sector mix varies significantly by region

The UK has the highest share of healthcare and financial sector PE deals, while Italy and Spain have the highest share of both consumer and industrial transactions in 2022. Both France and DACH have seen an increase of 50% in services sector share in 2022, driven across business models and subsectors from consulting to education.

The UK is still the most active PE investment region

Every region saw decreased PE deal activity in 2022. The UK remains the most active PE investment region by deal count and value, followed by France and DACH. DACH’s share of PE activity reduced in 2022 on the back of a less active industrial sector where a high proportion of sell-side mandates await to launch in 2023 on the expectation of greater macroeconomic clarity. On the other hand, Italy’s record share of 12% reflected successful sales of high quality international businesses in the industrial and consumer sectors. The closure of the IPO exit route increased the flow of Nordic M&A opportunities for private equity in 2022, increasing the region’s share of PE investment through secondary / tertiary buyouts.

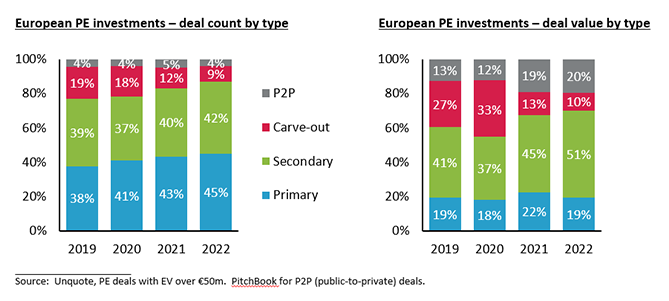

Primary and secondary buyouts continue to take share

Lower mid-market European PE firms are acquiring a greater share of companies directly from founders, family owners and management teams. Upper mid-market and large cap PE firms are acquiring more assets from other sponsors in secondary and increasingly tertiary buyouts. As the number of PE portfolio companies continues to grow, we expect this trend to continue. With no PE IPO exits in 2022, many of the larger portfolio companies opted for an exit to another PE buyer. 2022 was the first year where secondary buyouts accounted for over 50% of PE investments by deal value.

European P2P (public-to-private) M&A activity decreased in 2022 given Russia’s invasion of Ukraine, yet represented 20% of PE deployment value driven by a record average P2P deal size of over $2bn. Large deals included Atlantia (€19bn), HomeServe (£4bn), Euromoney (£1.6bn), Clinigen (£1.3bn) and Biffa (£1.3bn). P2P activity in 2022 was driven by lower (thus more attractive) public company valuations and a willingness by large-cap sponsors to deploy dry powder on bigger targets. The UK led activity in Europe, followed by the Nordics. P2P activity in 2023 is unlikely to match 2022 given the lower availability and higher cost of debt financing, particularly for multi-billion-dollar deals.

End of “cheap money” – higher cost and lower availability of debt financing

2023 will be a year of transition for private equity as the era of “cheap money” comes to an end. Debt financing is now nearly twice as expensive, driven by higher base rates and margins from lenders (to compensate for increased risk). Lenders are demanding a sufficient “equity cushion”, asking PE firms to contribute over 50% equity on most LBOs.

2022 represented the lowest new issuance in European public debt markets in the last 10 years with activity in Q4 2022 limited to selected refinancings, amend & extends and add-ons. A recovery in large-cap LBO deal momentum can begin once the syndicated loan markets open more broadly. The syndication backlog was largely cleared at the end of 2022 and secondary prices showed signs of stabilising, providing a helpful backdrop for syndication pricing in 2023.

The dislocation in public debt markets accelerated the penetration of private credit across Europe. By Q2 2022, debt funds were financing large-cap PE deals through unitranche clubs, partially filling the void left by public debt markets. In H2 2022, private debt markets became more selective, with appetite primarily for exceptional credits or from incumbent lenders. Incumbent lender support and portable facilities are becoming more important for new deal financing as macro uncertainty remains at the start of 2023. We have seen leverage levels fall by up to 1.0x or 1.5x EBITDA now relative to before Russia’s invasion of Ukraine. Base rate rises have pushed overall unitranche interest cost to ~10%, which may limit debt capacity for most credits to ~5x EBITDA given “acceptable” 2x interest cover.

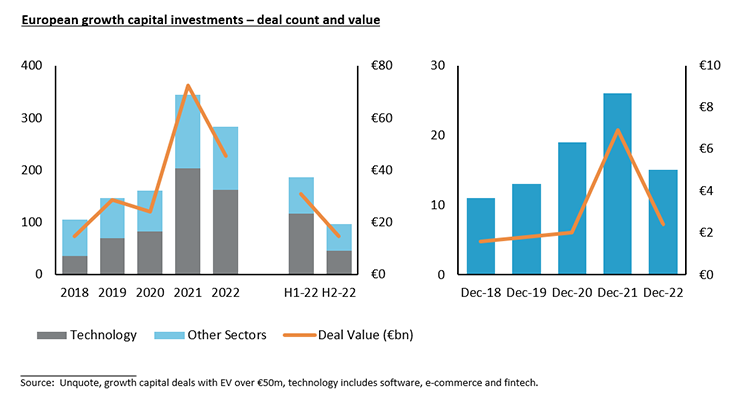

Decline in growth capital activity similar to PE market

Like European mid-market PE activity, growth capital deal count in H2 2022 was down almost 50% compared to H1 2022. Unlike mid-market PE activity, the share of technology for growth capital deals has meaningfully reduced. Following the reset in Big Tech public equity market valuations, growth equity investors are targeting companies with positive cash flow or minimal burn. Investors are shying away from earlier stage technology companies where an attractive LTV / CAC (Customer Lifetime Value to Customer Acquisition Cost) ratio still needs to be proven.

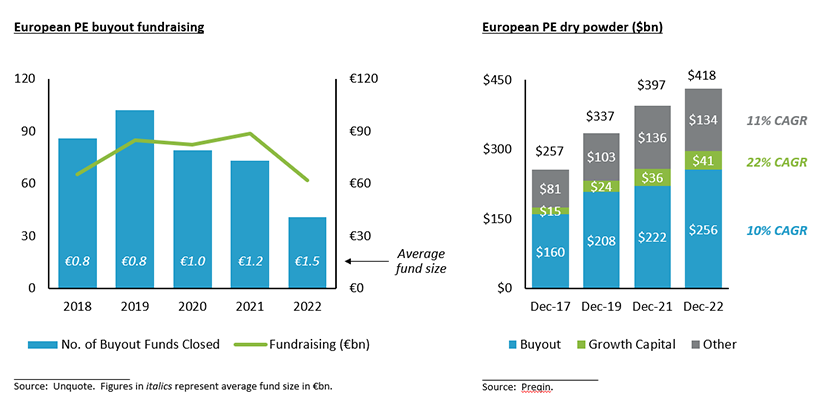

PE fundraising continued in 2022, but was 30% down from 2021

European buyout firms continued to raise larger funds with the average fund size reaching €1.5bn in 2022, almost double pre-Covid. €62bn was raised in 2022, 30% down from 2021 which benefitted from pent-up demand post Covid lockdown. Some mid-market GPs struggled to raise their target amount in 2022 due to a congested fundraising market and LP reallocation of capital to balance their private market exposure following the sell-off in public equities. The fundraising market continued to bifurcate as larger PE funds took a bigger share of LP commitments.

LPs want to see a track record of recent successful exits, which is in part driving some PE firms to exit selected high quality assets in trickier macro conditions during H2 2022 and Q1 2023. With record levels of PE dry powder, most GPs cannot sit on the side-lines as pressure to deploy capital remains throughout this downturn, especially considering that PE investments made during past periods of economic weakness (e.g. 2009) demonstrated superior returns.

Reliance on strategic and operational work (rather than multiple expansion) to create value

The low interest rate environment since the GFC (Great Financial Crisis) and through Covid increased asset prices, including PE portfolio companies, many of which benefitted from significant multiple expansion during a hold period of just a few years. With no expectation of multiple expansion over the next few years, PE firms are shifting to more strategic and operational work to generate that value. As such, we expect that buy-and-build activity will continue in 2023, though it could be constrained by debt capacity given the overall increase in interest cost at PE portfolio companies. In recent years, we have seen a contraction of hold periods, often as short as 3 years for top-quartile assets. We are likely to see the beginning of the return of 4 – 6 year hold periods as longer times are needed to generate value before crystallising gains.

Strong M&A backlog could drive a recovery in PE activity later in 2023

Reaching inflexion points for the macroeconomic outlook and public equity and debt markets could accelerate PE M&A later in 2023 (similar to H2 2020), unlocking a large supply of targets, many of which are already mandated. A high proportion of sale processes that were earmarked for 2022 have moved into 2023, where targets can evidence robust 2022 financial performance before launching into the M&A market. Relatively strong mid-market sell-side pitch activity in H2 2022 has built a pipeline of mandates for 2023, though many of these processes have also yet to launch. We are therefore seeing an M&A backlog that is “piling up” without a corresponding level of consummated deals in Q1 2023.

The latest economic forecasts for Europe suggest that the Eurozone could avoid recession while the UK will likely fall into recession in 2023. Any recession within Europe is expected to be deeper than in the US given the impact of Europe’s energy crisis on consumer spending. A meaningful recovery in the European M&A market could therefore lag a potential M&A recovery in the US by one or two quarters, similar to prior economic downturns, including the GFC and Covid. We continue to monitor US PE activity and overall public market sentiment to see how PE deal momentum in Europe could potentially follow suit.