Download the PDF version Download the PDF version

Baird Advisors Fixed Income Market Commentary

May 2009

|

|

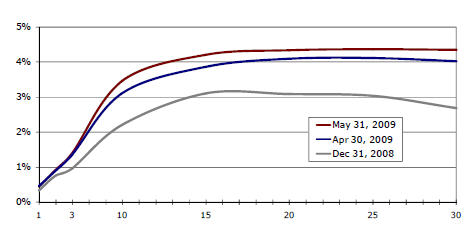

Long Treasury Yields Continue to Rise

|

Treasury yields continued to rise in May as heavy new issuance began to weigh on the bond market. During the month, the Treasury auctioned a stunning $770 billion of T-bills (maturities of less than 1 year) and $172 billion of T-notes and T-bonds (maturities of 2 to 30 years). Amazingly, the market absorbed all the new T-bills with no noticeable impact as 1-year T-bill rates fell by 2 bps in May. However, the increase in longer-term yields (10-year and 30-year yields rose 34 and 31 bps respectively) reflects the market’s concern that heavy supply will push interest rates higher over time. |

Treasury Yield Curve Comparison

Source: Bloomberg |

Click for larger view

|

Maturity |

Dec 31, 2008 |

Apr 30, 2009 |

May 31, 2009 |

1 mo. change |

YTD Change |

1 |

0.34% |

0.45% |

0.44% |

-0.02 |

0.10 |

2 |

0.76% |

0.90% |

0.92% |

0.02 |

0.16 |

3 |

0.97% |

1.36% |

1.40% |

.0.04 |

0.43 |

5 |

1.55% |

2.01% |

2.34% |

0.33 |

0.79 |

10 |

2.21% |

3.12% |

3.46% |

0.34 |

1.25 |

30 |

2.68% |

4.03% |

4.34% |

0.31 |

1.66 |

|

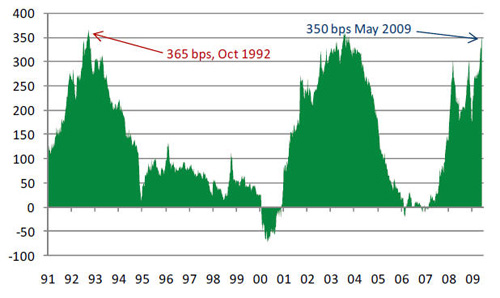

Yield Curve Approaches Record Steepness

|

With the recent increase in long-term Treasury yields, the difference between 2 and 30-year yields (350 bps on May 22) is approaching its all-time high of 365 bps reached in October 1992 (see chart at right). With Fed policy “wide open” for the time being, we believe a steep curve is part of the Government’s plan to aid bank earnings and feel it is likely that the yield curve will steepen further to a new record this year.

|

2 to 30 Year Yield Spread (in bps)

|

Spread Sectors Continue to Rally

|

As Treasuries lost additional ground in May (-1.01%,

-4.10% YTD), non-Treasury sectors continued to rally. Asset-backed securities continued their convincing recovery and led all investment grade sectors with another strong month (+5.43%, +14.90 YTD) followed by investment grade corporates (+3.90%, +5.44% YTD). Steady investor demand pushed municipals higher again in May (+1.06%, 7.43% YTD) and high yield bonds continued an impressive bounce with stocks (+6.73%, +26.80% YTD). Government Agencies (+0.01%, -0.20% YTD) and Agency MBS (+0.29%, +2.79% YTD) took a breather in May as investors favored higher yields over Government guarantees and TIPS advanced further (+2.10%, +5.73% YTD) on concerns that inflation could be the bond market’s next big problem down the road.

| Total Returns of Selected Barclays Capital Indices and Subsectors |

Index/Sector |

May |

2009 YTD |

| BC Aggregate Index |

0.73% |

1.32% |

| BC Gov’t/Credit Index |

0.80% |

-0.30% |

| BC Int. Gov’t/Credit Index |

0.74% |

1.15% |

| BC 1-3 yr. Gov’t/Credit Index |

0.68% |

1.83% |

| US Treasury Sector |

-1.01% |

-4.10% |

| Gov’t Agency Sector |

0.01% |

-0.20% |

| Corporate Sector |

3.90% |

5.44% |

| MBS Sector |

0.29% |

2.79% |

| ABS Sector |

5.43% |

14.90% |

| High Yield Sector |

6.73% |

26.80% |

| Municipal Sector |

1.06% |

7.43% |

| TIPS |

2.10% |

5.73% |

|

Indices and subsectors are unmanaged and an investment cannot be made directly in an index or a sector . |